Brad Jakeman & Rini Greenfield, Co-Founders & Managing Partners, Rethink Food

Excerpt from September 2022 Newsletter

A recent report by Pitchbook generated wide media attention suggesting that Food Tech as a sector may be experiencing a slowdown. Let’s get into that first!

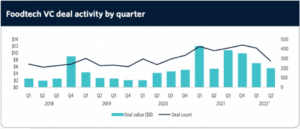

Pitchbook reported that in the second quarter of 2022, the overall transaction value for food technology venture capital decreased by nearly one-fifth, from $6.9 billion in the first quarter to $5.6 billion in the second. The fall in transaction value and the overall number of deals both fell in the second quarter of 2022 by 23%, from 359 funding deals in Q1 2022 to 275 deals finished in Q2.

The report goes on to highlight that the decrease in Q2 makes it the fourth consecutive quarter that funding for food technology has decreased. The total amount invested is down 45% ($4.5 billion) from the industry’s peak of $10.1 billion, which was set in the first quarter of 2021.

At Rethink Food, we remain extremely optimistic about FoodTech and believe that the trends outlined by Pitchbook can be explained by three main factors:

- A general cautiousness in venture investing overall given the current volatile and uncertain macro-economic, geo-political and public market environment. Food tech is not the only sector pulling back. In fact, relatively speaking, the sector’s quarter-over-quarter funding reduction is broadly in line with the 23% quarter-over-quarter decline in the venture capital market as a whole.

- The legacy food system is incapable of meeting society’s needs so disruption via FoodTech is inevitable and undeniably necessary. We believe deeply that disruption of the legacy food system is not only likely, but absolutely necessary to meet the needs of society moving forward. Why do we say this? Well, firstly, it’s a matter of simple supply and demand. Straight-lining the processes, practices and approaches we currently use to make, ship and sell food today into the future would require the deforestation of a land-mass twice the size of India in order to meet the food requirements of a population estimated to be 2 billion people larger[2]. This is not a viable solution. Secondly, the legacy food system currently represents one-third of the total Green House Gas Emissions[3] and 15% of all human-caused total emissions come from livestock agriculture[4]. With governments, investors, NGO’s, the activist diaspora and the private sector growing increasingly committed to curbing the global warming phenomena, it is simply impossible to effectively address Climate Change without significantly redesigning the way we produce our food.

- The definitional breadth of the “FoodTech” sector The Pitchbook report casts a very wide net in its definition of “FoodTech” to include many sub-sectors such as grocery “e-tailing”, premium in-home meal preparation and a number of other industry verticals which fall outside of Rethink Food’s investment mandate. When we look at the areas of our investment focus such as the Alternative Protein sub-category, we see that it has fared better than the entire FoodTech market (as defined by Pitchbook). According to the Good Food Institute[1], financing for alternative proteins fell by only 9% quarter over quarter ($833 million in investments, compared to $914 million in Q1), less than that of the total venture market and the broader food technology sector. With companies like Upside, Impossible, Eat Just, and others, Alternative Protein has seen its share of late-stage, high-value transactions. This trend appears to have continued into the most recent quarter. The fact that it has continued to get investment in each of the three key sub-segments (plant-based, precision fermentation and cultivated/cell-based) may have further contributed to its relative durability. We do believe that the market for plant-based meat is the one most likely to experience a short-term slowdown as it is proving to be both competitive and, in certain circumstances, difficult for some businesses to retain repeat consumers due to taste, price and nutritional profile. We remain confident that technology and ingredient unlock to solve for taste and nutrition in particular, together with some consolidation are likely to return this sub-sector to growth in the medium-term.

FoodTech—A broad sector with attractive pockets of growth fueled by ESG

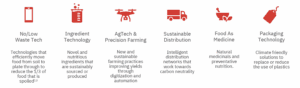

We believe that FoodTech will continue to attract investment interest in the sectors our analysis and thesis have identified as the most disruptive and likely to grow:

Most of these sectors (e.g. Ingredient Technology/Alternative Proteins) are accepted by many climate investors and may very well act as a protective factor in terms of the investment rates discussed earlier. According to the Goldman Sachs report ESG Tracker, public equity funds saw net withdrawals of $33 billion in April and May 2022, while public equity ESG funds experienced inflows of $14.7 billion. The star of erratic equities flows continues to be ESG. Alternative protein businesses for example can attract ESG-focused investors for funding in the near future as a result of the increasing importance of ESG factors in investment decisions and the mounting evidence that Alternative Protein investments are essential to making progress on climate change.

According to a recent report by Boston Consulting Group (BCG)[5], investments in plant-based proteins save the most CO2e per dollar of invested capital of any industry. However, “despite the favorable economics and attractive potential, including ready consumer interest, investment in sustainable foods is only a fraction of that committed to other sectors.”

For these three reasons, we anticipate future food investors to remain positive, particularly as government funding begins to be directed to the alternative protein industry. With the effects of the armed conflict in Ukraine negatively impacting the global food supply, governments around the world are starting to see FoodTech as a crucial component of national security strategy. While the US is lagging behind in that regard (food was not a major component of the recently passed, Inflation Reduction bill) we are starting to see state governments begin to invest in the space. Although the alternative protein sector hasn’t had the same level of public backing as the alternative energy sector, moderate future increases in government funding could spur further private investment in the sector.